Gold’s not been a profitable investment for some time now. Not for most ‘Stateside buy-and-holders, that is. Basis the London morning fix, gold’s average dollar price slumped 15.2 percent in 2013 and another 10.2 percent in 2014. This year’s not shaping up much better. Through May, gold’s mean price is 4.4 percent lower than last year’s.

Thus, it came as no surprise when Direxion Investments announced the closing of its Daily Gold Bull 3x Shares (NYSE Arca: BAR) ETF last week. The firm plans a wind-up and liquidation of the tiny $2.9 million fund by June 26.

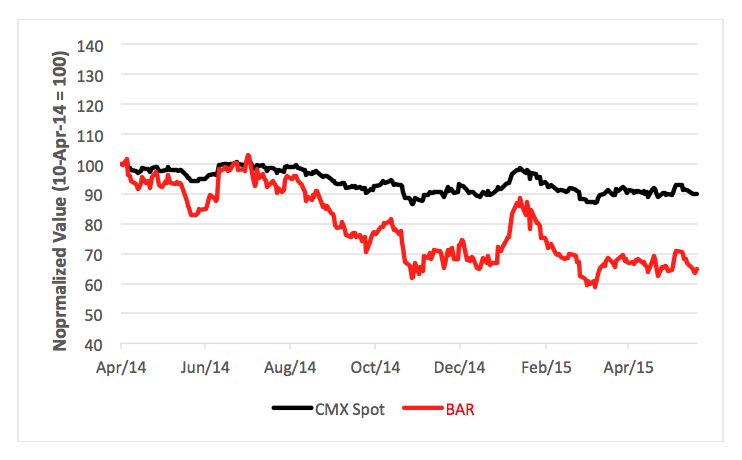

Since its April 2014 debut, BAR’s aimed to provide three times the daily return of the active front-month COMEX gold futures contract. To date, BAR’s done just that. Divide the standard deviation of BAR’s daily returns by that of the COMEX spot month and, voilà, you end up with a quotient of 3. You don’t however, get three times the COMEX cumulative return with BAR. From its inception, the fund’s market price has sunk 35.2 percent while the metal’s spot price dipped only 9.9 percent.

{kind=link}

BAR, of course, isn’t the only bullish gold play underwater. Of 15 exchange-traded products tracking the metal’s price over the past 12 months, only two are in the black.

Two in the black? Even as gold, the funds’ only asset, declined? How’s that?

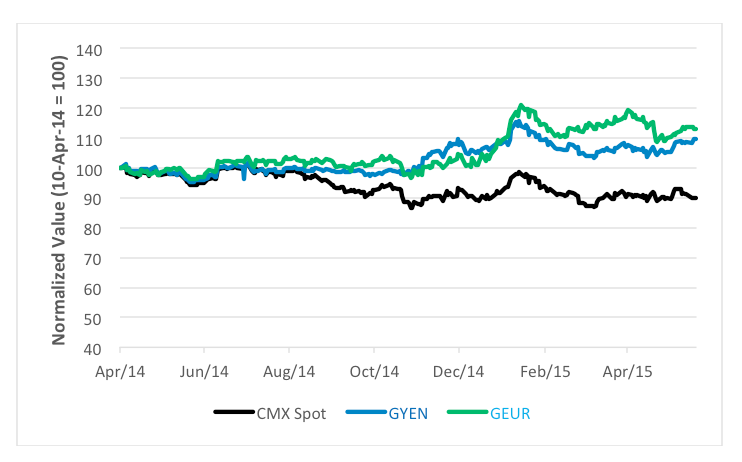

To answer that question, you have to refine the meaning of “asset.” A horde of gold is certainly an asset. But its real value depends on the currency that’s used to meter its worth. Gold purchased in dollars is one kind of asset; metal bought with yen or euros is something else.

AdvisorShares’ Gartman Gold/Euro ETF (NYSE Arca: GEUR) and its sibling Gartman Gold/Yen ETF (NYSE Arca: GYEN) both finance gold in their named currencies through the forwards or futures markets. Doing so insulates their positions from the deleterious effects of a resurgent greenback – one of bullion’s biggest bugaboos.

That strategy’s certainly worked well recently. Against COMEX’s 9.9 percent loss, GYEN actually gained 9.7 percent while GEUR rose 13 percent. Credit a 22 percent climb in the U.S. Dollar Index for the assist.

{kind=link}

Gold, for many, is essentially an anti-dollar play. The Gartman funds afford these gold bulls a hedge and a reason to party while dollar-dependent investors cry into their beers.

Brad Zigler is REP./WealthManagement's Alternative Investments Editor. Previously, he was the head of marketing, research and education for the Pacific Exchange's (now NYSE Arca) option market and the iShares complex of exchange traded funds.