Tax planning professionals need to master the skill of communicating the tax savings from the use of a planning technique in a manner that a potential client can quickly and easily understand. Part of an effective communication process is to give the client specific examples to compare with each other. Another part involves avoiding the use of technical terms with which the client is often unfamiliar. This is particularly true when dealing with charitable giving strategies. Here are some tips on communicating the benefits of a charitable lead annuity trust (CLAT) to a client.

Use of Introductory Statements

When charitable giving is involved, a simple introductory statement to use when you first meet a potential client can be something like this:

With a properly structured charitable giving technique, what you can end up giving to charity need not cost you anything. Instead, what can be given to charity is the money you would have otherwise paid in federal and state income taxes and estate taxes.

Before starting to describe the possible planning technique, you can expand on this introductory statement by mentioning some key benefits:

1. Pass assets to the next generation without any transfer taxes. By using a lifetime CLAT, especially in today’s low interest rate environment, you can pass an income-producing investment asset on to the next generation without any gift or estate taxes.

2. Assign income to another taxpayer. There are income tax advantages to using a CLAT by assigning taxable income to another taxpayer, especially if the assignee taxpayer is in a lower income tax bracket.

3. Individuals with short life expectancies can take advantage of the estate-planning compounding over a longer term. For individuals in their late 80s and 90s, using lifetime CLATs for fixed terms can extend the annual compounding for as many years as needed after their deaths so that there are no gift or estate taxes on the transfer of an income-producing asset to the next generation.

CLATs

A CLAT works the same way as a grantor retained annuity trust (GRAT), except the annual annuity is given to charity instead of retained by the trust creator. Because there’s no retained annuity interest, and if the remainder interest is gifted away at formation, there’s no exposure to estate tax inclusion if the creator of the CLAT dies during the CLAT term, as there is with a GRAT. It’s the use of financial leverage (the assumption that the investment rate of return is greater than the Internal Revenue Code Section 7520 rate) and the compounding of that financial leverage over a long period that produce favorable results. The lifetime CLAT with a fixed term is an ideal vehicle to take advantage of the compounding over a long period of time, as the CLAT term can continue after the individual dies.1

Four Scenarios to Present to Client

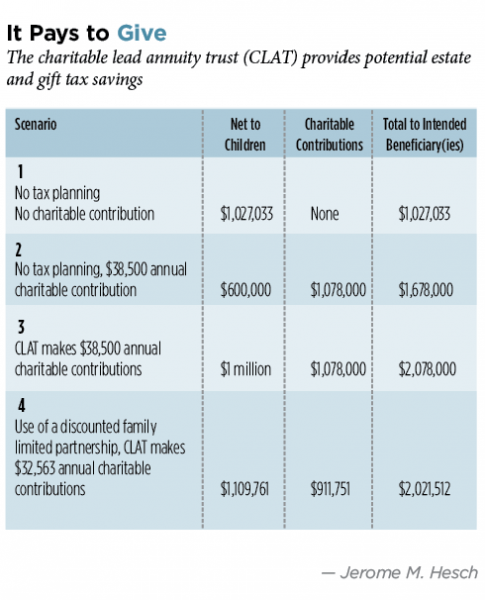

Below are four scenarios using a $1 million income-producing asset and the net results under each.

To illustrate the tax savings to a client, start with a situation in which the client hasn’t implemented any tax plan so that she can compare the benefits from the various planning techniques.

The following example uses a lifetime CLAT to illustrate how to accomplish the communication objective in a brief amount of time without the use of technical terms. Remember, it’s always easier to communicate by the use of examples!

Assume that your client, Senior, a resident of California, a state with a top 13.3 percent income tax on individuals,2 with little or no charitable intentions, owns a $1 million portfolio of corporate bonds, paying $38,500 of annual interest (a 3.85 percent return). The current gift tax rate is 40 percent. The September 2016 IRC Section 7520 rate is 1.4 percent.3 You can present Senior with the following four scenarios to help her understand and reach the right conclusion.

Scenario 1: Senior retains the $1 million investment portfolio, earning 3.85 percent annually, pays the federal and state income taxes on the $38,500 of ordinary income each year and allows all earnings, after the payment of the income taxes, to accumulate as part of this investment portfolio. Assume that the accumulated income also earns the same 3.85 percent rate of return. At the end of 28 years, the investment fund will grow to $1,711,722. Senior gifts the entire $1,711,722 of accumulated funds directly to her children. After the payment of $684,689 in gift taxes, computed at the 40 percent gift tax rate, the children effectively net $1,027,033.4

Scenario 2: Each year, Senior gifts the entire $38,500 of annual investment income to charity, creating a charitable deduction that offsets the interest income. Senior gifts the $1 million investment portfolio to her children at the end of 28 years. The children effectively net $600,000 after the payment of gift taxes at the 40 percent rate, and the charity receives a total of $1,078,000 over the 28-year period.

Scenario: 3: Senior contributes the $1 million investment portfolio to a lifetime CLAT, which in turn is required to distribute a fixed annuity of $38,500 to charity each year over a 28-year period.5 Because the value of the remainder interest to Senior’s children is zero6 (hence, the term a “zeroed-out CLAT”), there’s no taxable gift at the time the trust was created. At the end of 28 years, the CLAT terminates and distributes all $1 million to the children without incurring any gift taxes. Therefore, the children net $1 million, and the charity receives the same $1,078,000 over the 28-year period.

A client who’s already giving substantial amounts to charity each year in her individual capacity can’t avail herself of the estate and gift tax savings from a lifetime CLAT. If this client will be continuing similar annual charitable donations, she should use a lifetime CLAT to also obtain the transfer tax savings.

Scenario 4: Senior contributes the $1 million investment portfolio to a family limited partnership (FLP). After taking a conservative 25 percent valuation discount, Senior contributes the discounted LP interest, valued at $750,000, to a CLAT, which is required to pay $32,563 annually to charity over the 28-year CLAT term.7 Over the 28-year period, the charity receives $911,751. And, on termination of the CLAT, it distributes $1,109,761 to the children, free of all gift taxes.

Comparing the Scenarios

By having the CLAT make the annual charitable contributions under Scenario 3, a client can pass almost as much to her children than by doing no tax planning and still give over $1 million to charity.8 A client who’s already making significant individual charitable contributions and who uses the CLAT for the same charitable giving can take advantage of the potential gift and estate tax savings that the CLAT provides.

Comparing Scenario 1 (no giving) with Scenario 3 (CLAT makes contributions), the total of $1.078 million in annual distributions to charity only costs the client $27,033.9 (See “It Pays to Give,” p. 62.) The client is giving to charity the practical equivalent of the gift taxes she would have otherwise paid if the CLAT hadn’t been used. Even though the client’s children would have been slightly better off under Scenario 1, the client may still be interested in the CLAT if you explain that the $27,033 reduction in the amount the children net is the practical equivalent of it only costing the family $27,033 to give $1,078,000 to charity over a 28-year period.

By using an FLP, as illustrated in Scenario 4, the transfer tax savings show that the client’s children can be better off than under Scenario 1. Now, the client can give the children $82,728 ($109,761 less $27,033) more and still give $911,751 to charity.

Be aware that the use of the CLAT produces this favorable result only because of the historically low Section 7520 rate. At a higher Section 7520 rate, the same $38,500 annual annuity needed to zero-out the CLAT that wouldn’t deplete principal would require a term longer than 28 years.10 An alternative is not to zero-out the CLAT, so that there’s a value for the remainder interest passing to the children as a taxable gift. Any gift taxes on that taxable gift can be offset by the client’s remaining gift tax exemption, if available.

The client may be reluctant to postpone the distribution to the children by 28 years. If the client wanted to create a 20-year CLAT using the 1.4 percent Section 7520 discount rate, distributing only the $38,500 of annual bond interest to charity, the value of the remainder interest would be $332,445, and the client would have to report that amount as a taxable gift at the time the CLAT was funded.

If the income-producing asset was generating a greater rate of return than the 3.85 percent available from the bond portfolio, then the CLAT term can be shorter than 28 years to zero-out the CLAT. For example, if the investment portfolio was generating a 5.768 percent rate of return ($57,680 annual income), then the CLAT term need only be 20 years for a zero value remainder interest, and the entire $1 million of trust principal would pass to the children at the end of 20 years.

If the CLAT used a discounted LP interest valued at $750,000 with the same $57,680 annual income, the charitable annuity needed to zero-out the CLAT would only be $32,563. Thus, the actual income produced each year in excess of the charitable annuity could accumulate in the CLAT, and at the end of the 20-year term, the trust would have $1,109,761 to distribute to the children. Alternatively, if the annual charitable annuity was the entire $57,680 of investment income, the term needed to zero-out the CLAT would be 15 years.

Reducing an Individual’s AGI

Explain to the client that certain itemized deductions are phased out based on a percentage of the client’s adjusted gross income (AGI). By assigning taxable income to the CLAT, the client’s AGI is reduced. For example, the medical expense is reduced by an amount equal to 10 percent of AGI. Likewise, miscellaneous itemized deductions are reduced by an amount equal to 2 percent of AGI. All itemized deductions, except the medical and investment interest itemized deductions, are reduced by the 3 percent phase-out.11 The reduction in the personal exemption can also be reduced if AGI is reduced. Finally, the exposure to the alternative minimum tax (AMT) is based on an individual’s level of income. Your client may be able to reduce the impact of the AMT if taxable income can be assigned to another taxpayer.

If your client can reduce gross income, it’s possible to reduce, and sometimes eliminate, these phase-outs of deductions. Therefore, assignment of income to another taxpayer can be helpful even if the assignee taxpayer isn’t in a lower marginal income tax bracket.

Clients who make recurring and predictable annual charitable donations, and take their charitable income tax deductions on their individual income tax returns, are missing the opportunity that the CLAT provides by shifting the income used to make their charitable contributions to another taxpayer. With the historically low Section 7520 rate (1.4 percent can be used for September, October and November 201612), a non-grantor CLAT for a fixed term can be designed to structure the annual annuity to charity for a much shorter fixed term than if the Section 7520 rate was higher.

Further Benefits

The above analysis assumed that the CLAT wasn’t a grantor trust. As a separate taxpayer for federal income tax purposes, the non-grantor CLAT reports both the taxable income and the charitable deduction each year. Although the individual who created the non-grantor CLAT is able to use the charitable gift tax deduction, the individual can’t take an income tax charitable deduction with a non-grantor CLAT.

If the CLAT is a grantor trust, the individual receives a current charitable income tax deduction equal to the present value of the charitable annuity payments, but is required to report the CLAT’s annual income without a further income tax charitable deduction. However, there’s an additional gift and estate tax benefit with the grantor CLAT. As a grantor trust, the grantor must report and pay income taxes on the CLAT’s entire taxable income even though there’s no further charitable income tax deduction. By paying the income taxes on the grantor CLAT’s taxable income, the tax payments reduce the client’s retained assets that would otherwise be exposed to the estate tax.

Comparisons Are Key

When you’re explaining the estate and gift tax advantages of the CLAT to a potential client, keep in mind you should try to explain how the tax savings are achieved without ever referring to the IRC and without using technical terms. The phrase “zeroed-out CLAT” isn’t something the client will initially understand. The use of simple numerical illustrations that first show what the family would net with no tax planning and then compare the amount received by the next generation with the implementation of the tax plan is the most effective way to communicate. And, examples comparing the scenarios illustrated above can communicate the tax savings within the first 10 to 15 minutes of the client meeting. Remember, what the client really wants to know during the first meeting isn’t how the planning technique works, but how much in taxes she can save!

Endnotes

1. For purposes of simplicity, the charitable lead annuity trust (CLAT) won’t be a grantor trust. Instead, the CLAT will be a complex trust treated as a separate taxpayer for federal income tax purposes. Therefore, each year, the CLAT will report its income, and each year, the CLAT is entitled to its own charitable income tax deduction for each charitable annuity payment. Because the CLAT isn’t an individual, it can offset 100 percent of its taxable income with its charitable deduction. An individual who can’t fully use his charitable deductions because his charitable contributions exceed 50 percent of his adjusted gross income should consider assigning the charitable deduction to the non-grantor CLAT.

2. The combined federal income tax on interest income is 43.4 percent when the 3.8 percent net investment income tax (NIIT) is added to the regular

39.6 percent income tax rate. And, in a state like California, where the top state income tax rate is 13.3 percent, the effective rate is then 56.7 percent. In New York, the top state income tax rate is 8.82 percent, and the New York City rate is another 4.3 percent. All or a portion of the itemized deduction for state and local income taxes may be nullified by the Internal Revenue Code Section 68 phase-out for itemized deductions and more likely by the alternative minimum tax (AMT).

3. Revenue Ruling 2016-20. Charitable lead trusts not only can use the IRC Section 7520 rate for the month the trust is established, but also can use that rate for the two succeeding months. See Section 7520(a)(2).

4. The children actually receive the entire $1,711,722, but the gift taxes paid by the parent reduce the remaining amount that the parent can give to the children.

5. Each year, the trust reports the $52,240 as taxable income, and each year the trust is permitted to deduct the entire $52,240 as a charitable contribution.

6. Using the September 2016 1.4 percent Section 7520 discount rate, the present value of $38,500 a year for 28 years is $1 million. The value of the remainder interest is computed by subtracting from the value of the asset contributed to the CLAT ($1 million) the value of the annuity interest given to the charity ($1 million).

7. Using the 1.4 percent Section 7520 discount rate, the present value of $32,563 annually for 28 years is $750,000.

8. This illustration assumes that the client desires to give to charity. If the client has no charitable desires, then she may be able to transfer more to the children using another estate-planning technique, such as a grantor retained annuity trust. But, another objective is to encourage clients who may not otherwise make charitable contributions to give to charity. We call that a “mitzvah!”

9. Had the individual directly given the same $38,500 each year to charity over a 28-year period, it would have cost the client only $17,055 each year (after taking into account the income tax savings for the annual $52,240 charitable deduction, assuming an effective federal and California income tax rate of 56.7 percent (39.6 percent regular tax + 3.8 percent NIIT surcharge + 13.3 percent state)) and assuming that the 3 percent phase-out of itemized deductions and the AMT don’t apply to the charitable itemized deduction.

10. If the CLAT term was for 39 years, the present value would be $1 million using a 2 percent Section 7520 discount rate.

11. The charitable income tax deduction isn’t exposed to the 3 percent phase-out if there are other significant itemized deductions, such as mortgage interest and state income taxes. But, the AMT applies to the charitable itemized deduction.

12. For CLATs, the Section 7520 rate can be the rate for the current month or the rates for the two preceding months.